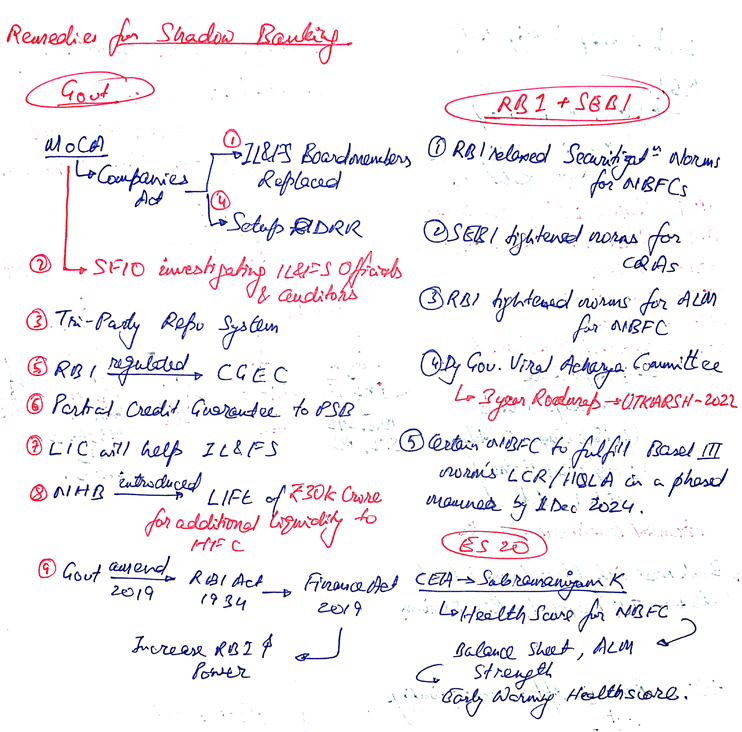

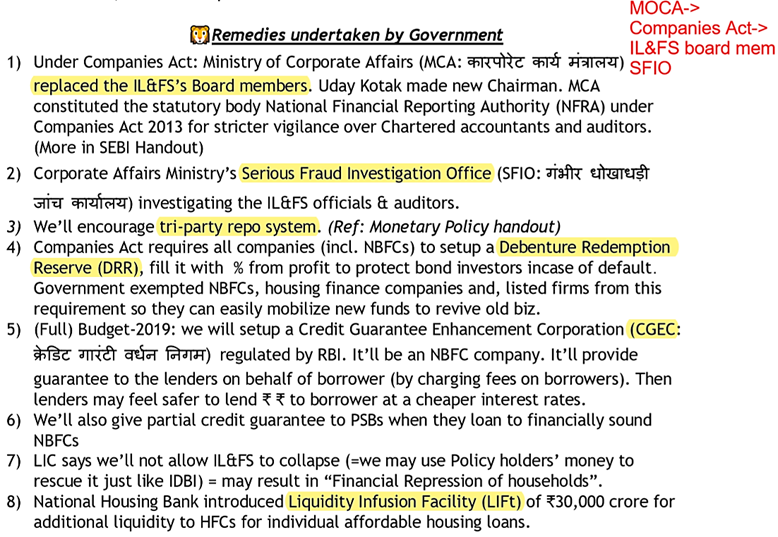

DRR= Debenture Reserve Ratio

Debenture– A long term security yielding fixed interest secured against some girwi.

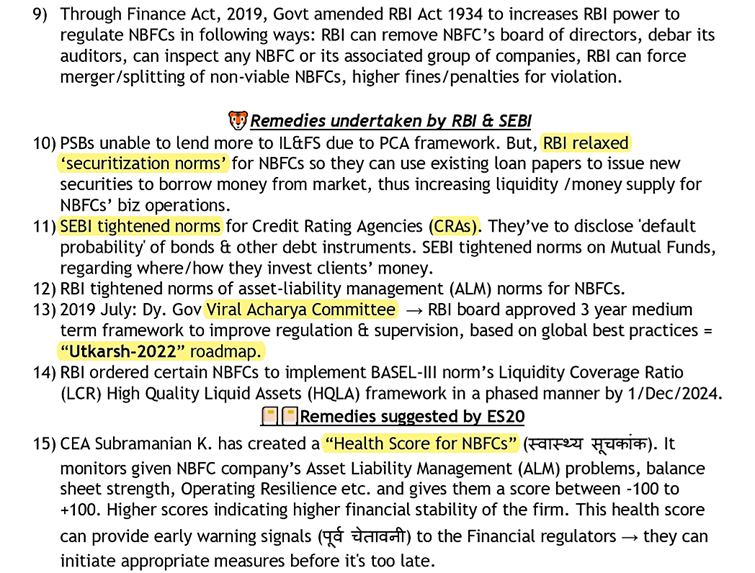

ALM= Asset Liablity Management

RBI–>CGEC= Credit Guarantee Enhancement Corporation– It’ll be an NBFC company. It’ll provide guarantee to the lenders on behalf of borrower (by charging fees on borrowers). Then lenders may feel safer to lend ₹ ₹ to borrower at a cheaper interest rates.

LIFt= Liquidity Infusion Facility

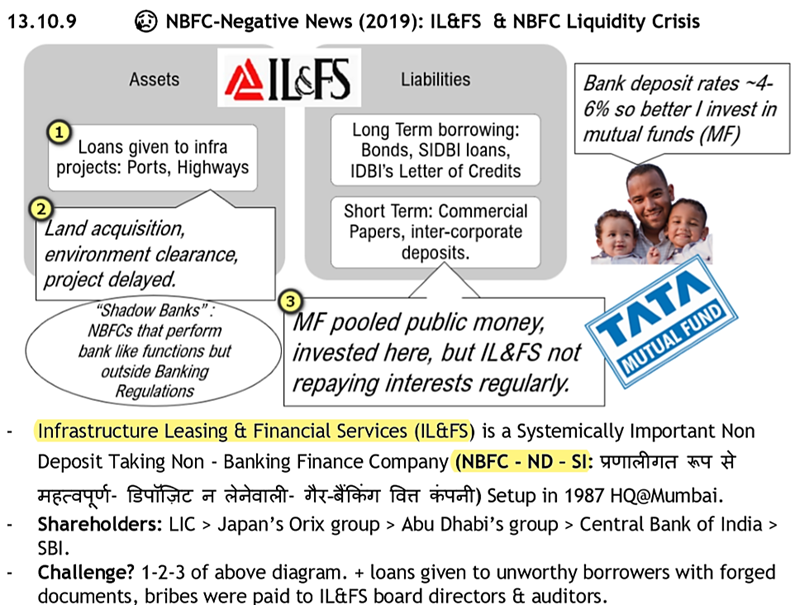

NBFC: Shadow Banking –>

ES20 Vo1 Chapter 08 on ‘NBFC’s Financial Fragility’ observed

- Shadow banking is a set of activities and institutions. They operate partially (or fully) outside the traditional commercial banking sector. They are not fully regulated by the RBI.

- A shadow banking system can be composed of a single institution or multiple entities forming a chain. They mobilize funds by borrowing from banks, issuing Commercial Papers (CP) and Bonds (Non-convertible debentures)

3 important segments of the shadow banking system in India

- HFCs=Housing Finance Companies. E.g. Dewan Housing Finance Limited (DHFL)

- LDMFs=ṭ Liquid Debt Mutual Funds invest clients money into short term debt instruments such as T-bill (of Govt) and Commercial Papers (of companies). e.g. certain schemes by UTI, Kotak, L&T, Tata mutual funds

2019: Some of these LDMFs had invested clients money in IL&FS and DHFL, but failed to get the money back. Nearly ₹4000 crore of investors’ money is stuck, triggering the NBFC crisis in India. - Retail-NBFCs –Retail Non-Banking Financial Companies such as Gold loan companies, asset finance companies etc.

Shadow banking system’s assets are risky and illiquid. If there is a ‘bank run’ like situation (depositors / investors demanding the money bank) these shadow banks can’t honour the obligations. As seen in the ILFS crisis (2019) →

Finance Minister in her Budget speech revived the idea of a ‘bad bank’ by stating that the Centre proposes to set up an asset reconstruction company to acquire bad loans from banks.

A bad bank is a financial entity (ARC) set up to buy non-performing assets (NPAs), or bad loans, from banks.

The aim of setting up a bad bank is to help ease the burden on banks by taking bad loans off their balance sheets and get them to lend again to customers without constraints.

RBI–> from 10lakh cr from 2018–> 9lakh cr in 2020.

The size of bad loan write-offs by banks has steadily increased since the RBI launched its asset quality review procedure in 2015, from around ₹70,000 crore in 2015-16 to nearly ₹2.4 lakh crore in 2019-20, while the size of fresh bad loans accumulated by banks increased last year to over ₹2 lakh crore from about ₹1.3 lakh crore in the previous year.

The Troubled Asset Relief Program, also known as TARP, implemented by the U.S. Treasury in the aftermath of the 2008 financial crisis, was modelled around the idea of a bad bank.

National Asset Reconstruction Company Ltd (NARCL), the name coined for the bad bank announced in the Budget 2021-22, is expected to be operational in June

AMC= Asset Management company

NCLT= National Companies Law Tribunal

NCLAT= National Companies Law Appellate Tribunal

DRT= Debt Recovery Tribunal

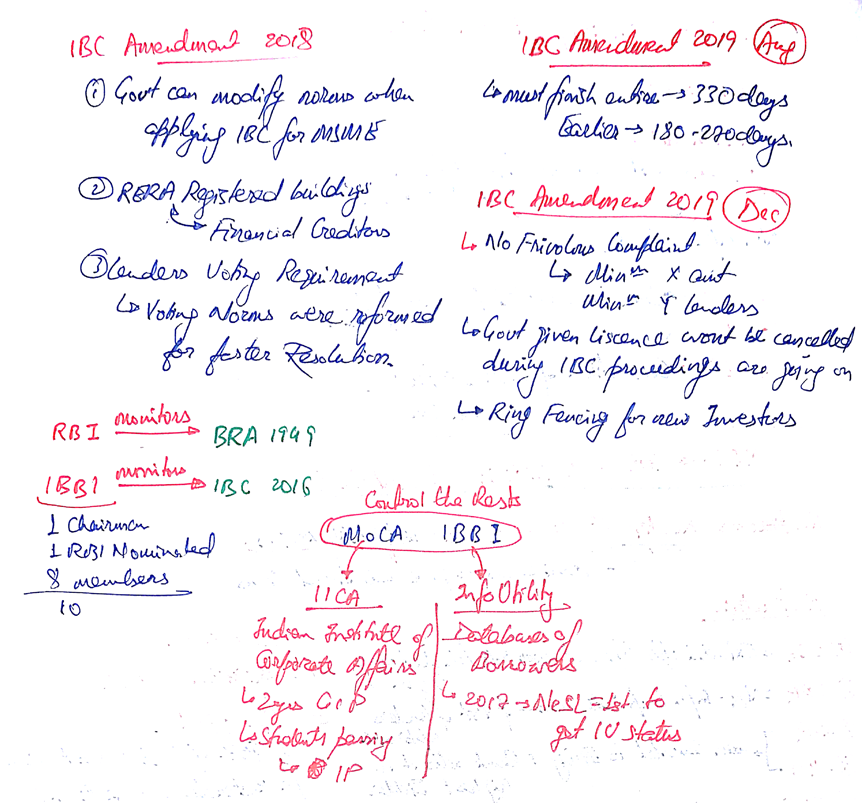

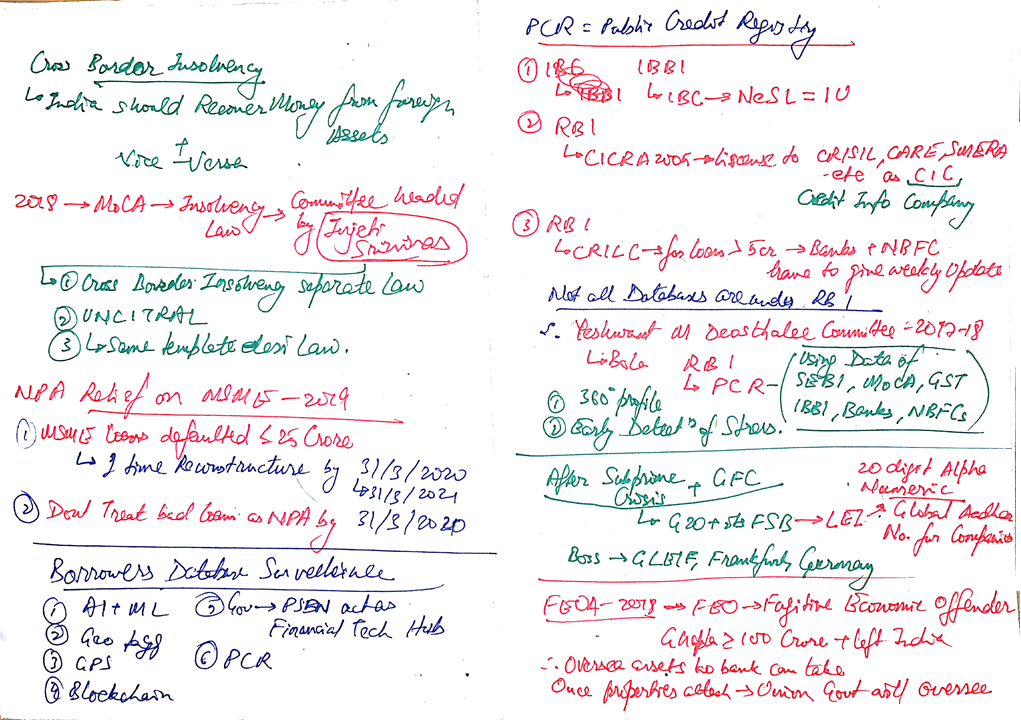

IBBI’s administrative control rests with the Ministry of Corporate Affairs (MCA).

MoCA–>IICA=Indian Institute of Corporate Affairs is an autonomous body

NeSL= National E-Governance Services Ltd

(owned by consortium of SBI, LIC etc.) was the first to get the IU status.

ICA= Inter-Creditor Agreement

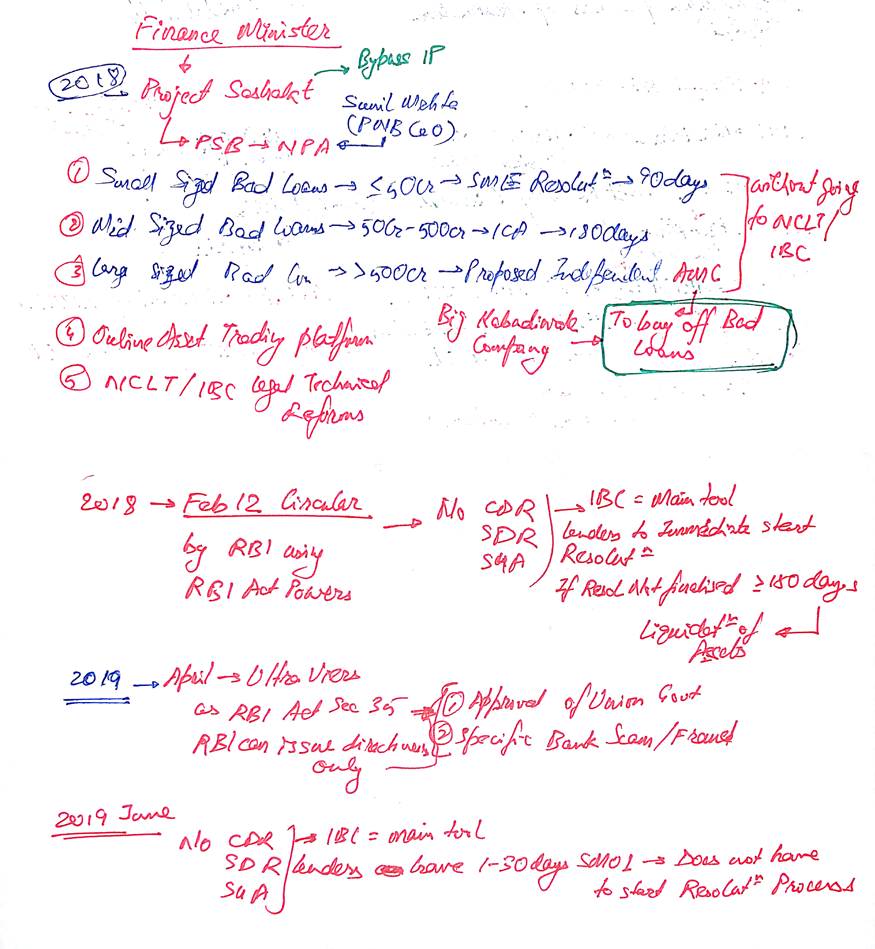

2019-June: Consequently, RBI released Prudential Framework for Resolution of Stressed Assets Directions 2019–

- RBI applied it on Banks, AIFI and selected categories of NBFCs- using the powers under Banking Regulation Act (1949) and RBI Act (1934).

- It discontinued CDR, S4A, SDR, JLF etc. henceforth IBC to be main tool.

- If principal / interest is overdue for 1-30 days, classify loan account as SMA-0. Then, within 30 days, the lender shall review the loan account, & initiate resolution process (RP). (Previous Feb-12 circular required lenders to start RP within 1-day of SMA-0.)

- It framed rules to facilitate Sashakt approach #1 and #2-inter-creditor agreement (ICA).

- Lenders must upload data of ₹5 crore /> loans to RBI’s CRILC portal on weekly basis.

- Forbids loan restructuring for borrowers who have committed frauds/willful default in

- past. Forbids evergreening of stressed loans.

SDR–> whatever loan taken.. the loan documents are shown and converted into shares–> then sold as equity–> gather money to solve NPA.

SARFAESI—

2020- SC–> coop banks have the power to use SARFAESI

Union made–> SARFAESI act–> power to banking sector= all banks

Economic Survey 2020-> on an avg–>

IBC took 340 days — SARFAESI took 4.3 yrs

IBC– faster resolution

50k crore worth of NPA accounts CONVERTED to std Asset ∴ Corporate behavior has improved.

Corona kand

Atmanirbhar–> RBI–>Loan Moratorium–> suspension of loan for 6months form March to Aug. Then loan must be paid.

If not paid for further 3 months (90days+) –> report it as NPA.

Therefore no NPA till Dec.

Atmanirbhar –> Also no new cases under IBC for 6 months

UNCITRAL= United Nations Commission on International Trade Law

CICRA 2005= Credit Information Companies Regulation Act

CRILC= Central Repository of Information on Large Credits