Taxing new spaces– to overcome the previous disadvantages of taxes

- Taxing new spaces

- GST revenues have decreased

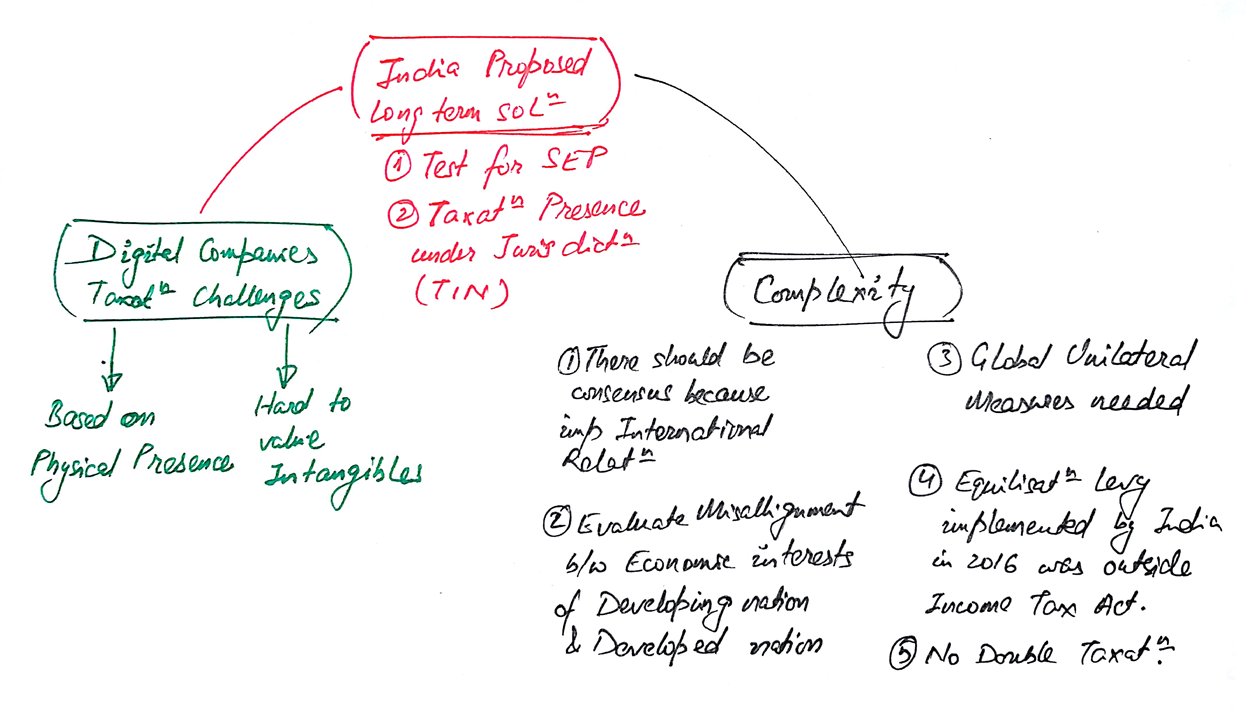

- The proliferation of technology has challenged the conventional notions

- 2 challenges with taxing Digital company

- tax business profit son physical presence- 1920

- Hard to value intangibles.. registred in low tax jurisdiction

- OECD-Organisation of Economic Development

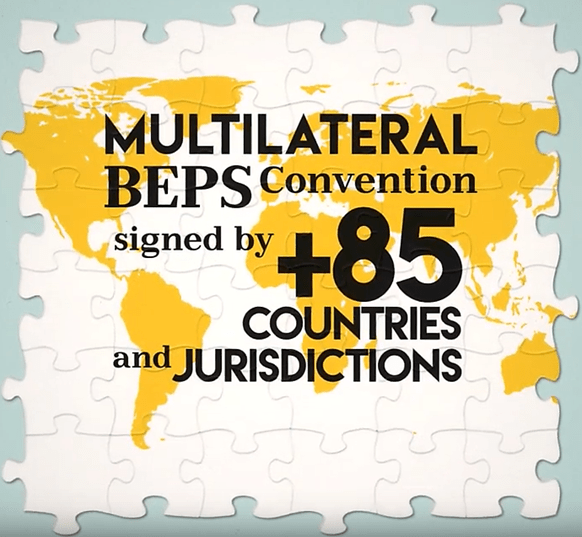

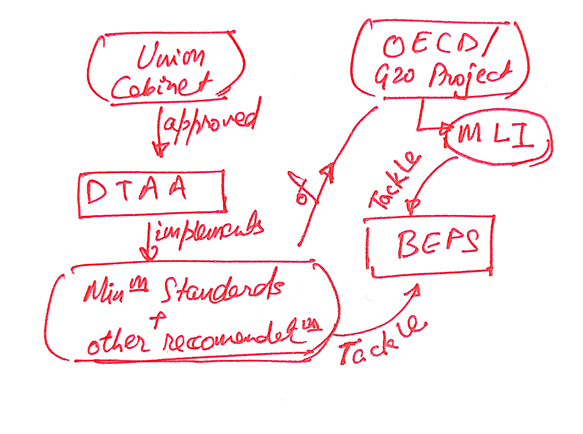

The government has ratified the international agreement to curb base erosion and profits shifting (BEPS)– Multilateral Convention to Implement Tax Treaty Related Measures, a bid to stop companies from moving their profits out of the country and depriving the government of tax revenue.

What is MLI?

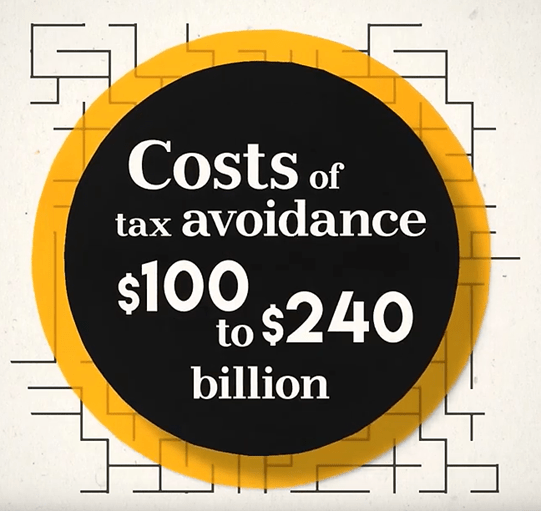

The Multilateral Convention (MLI) is an outcome of OECD or G20 Project to tackle Base Erosion and Profit Shifting (called as BEPS Project). BEPS means tax planning strategies which exploit mismatches and gaps in tax rules so as to artificially shift profits to a low or no-tax location where there is little/no economic activity, which further results in little or no overall corporate tax being paid.

What is BEPS?

Base erosion and profit shifting refers to the phenomenon where companies shift their profits to other tax jurisdictions, which usually have lower rates, thereby eroding the tax base in India

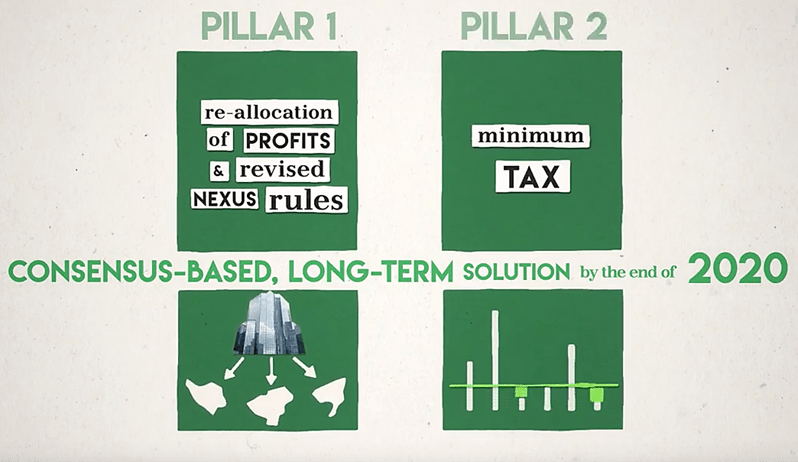

The Agreement and Protocol implements minimum standards and other recommendations of G-20 OECD Base Erosion Profit Shifting (BEPS) Project (or BEPS Project). The Agreement includes provisions such as a Principal Purpose Test, Preamble Text, a General Anti-Abuse provision along with a Simplified Limitation of Benefits Clause (SLBC) as per BEPS Project. This will result in curbing of tax planning strategies which exploit gaps and mismatches in tax rules.

Impact: MLI will modify India’s tax treaties that will help reduce revenue loss due to treaty abuse and Base Erosion and Profit Shifting (BEPS) strategies by ensuring that profits are taxed where ever substantive economic activities generating profits are carried out.

India’s DTAA with MLI shall get modified in following prominent ways-

- MLI will modify their application in order to implement BEPS measures. It will be applied alongside existing tax treaties.

- Avenues leading to avoidance of capital gains from alienation of shares or interests which derive value principally from immovable property would be plugged.

- Some dividend transfer transactions that are intended to lower withholding taxes payable on dividends artificially would also be prevented.

- As on date out of 93 CTAs notified by India, 22 countries have already ratified MLI and so DTAA with these countries will be modified by MLI.

- Once MLI comes into effect, India’s DTAA will have a new Preamble and Principal Purposes Test (PPTs).

- These changes would also lead to curbing of artificial avoidance of Permanent Establishment (PE) status through various arrangements.

Way Ahead: MLI will enter into force for India on 1 October 2019 and provisions enshrined in framework will come into effect on India’s DTAAs from fiscal year 2020-21 for bilateral tax treaties.mpact: MLI will modify India’s tax treaties that will help reduce revenue loss due to treaty abuse and Base Erosion and Profit Shifting (BEPS) strategies by ensuring that profits are taxed where ever substantive economic activities generating profits are carried out.