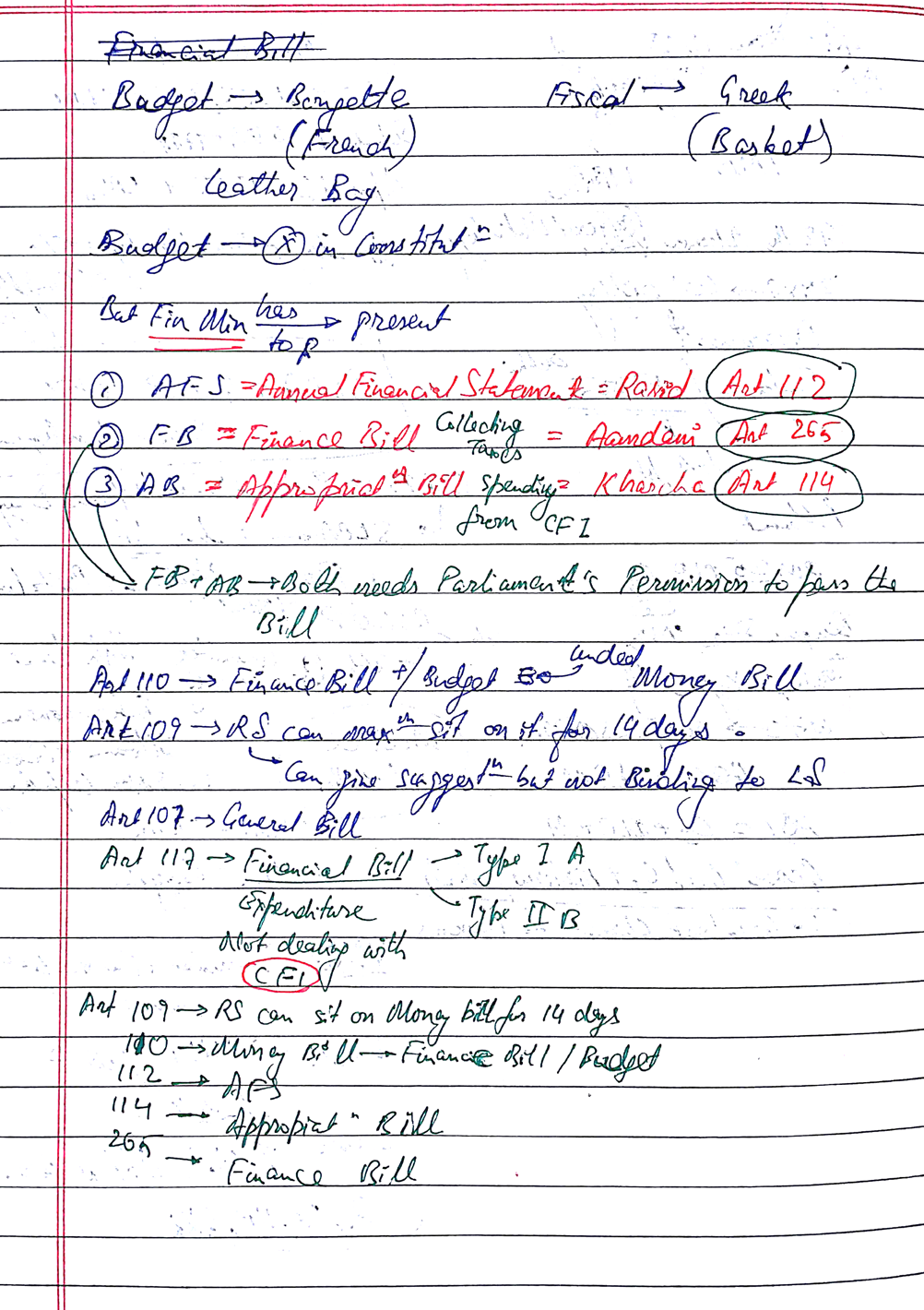

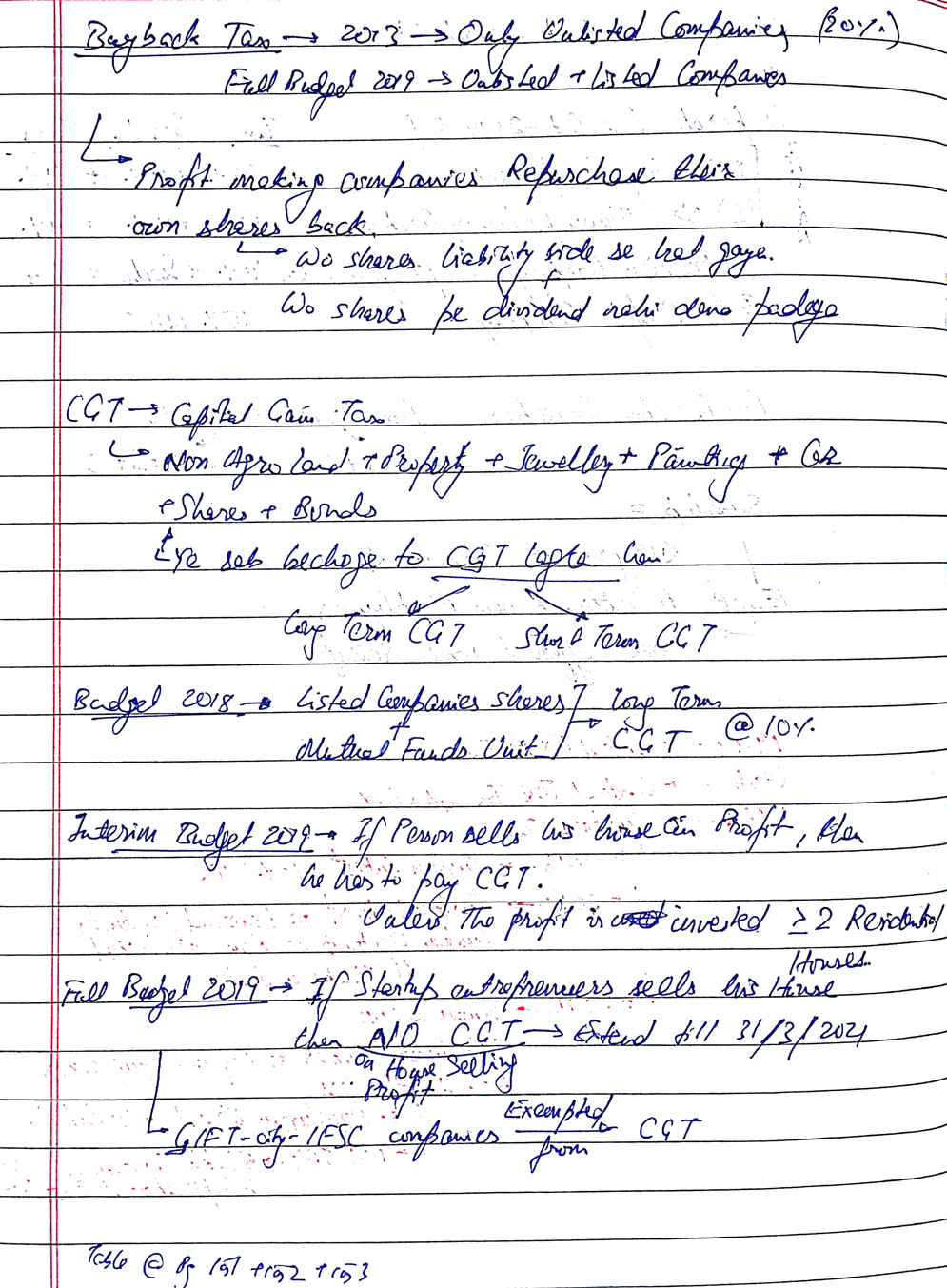

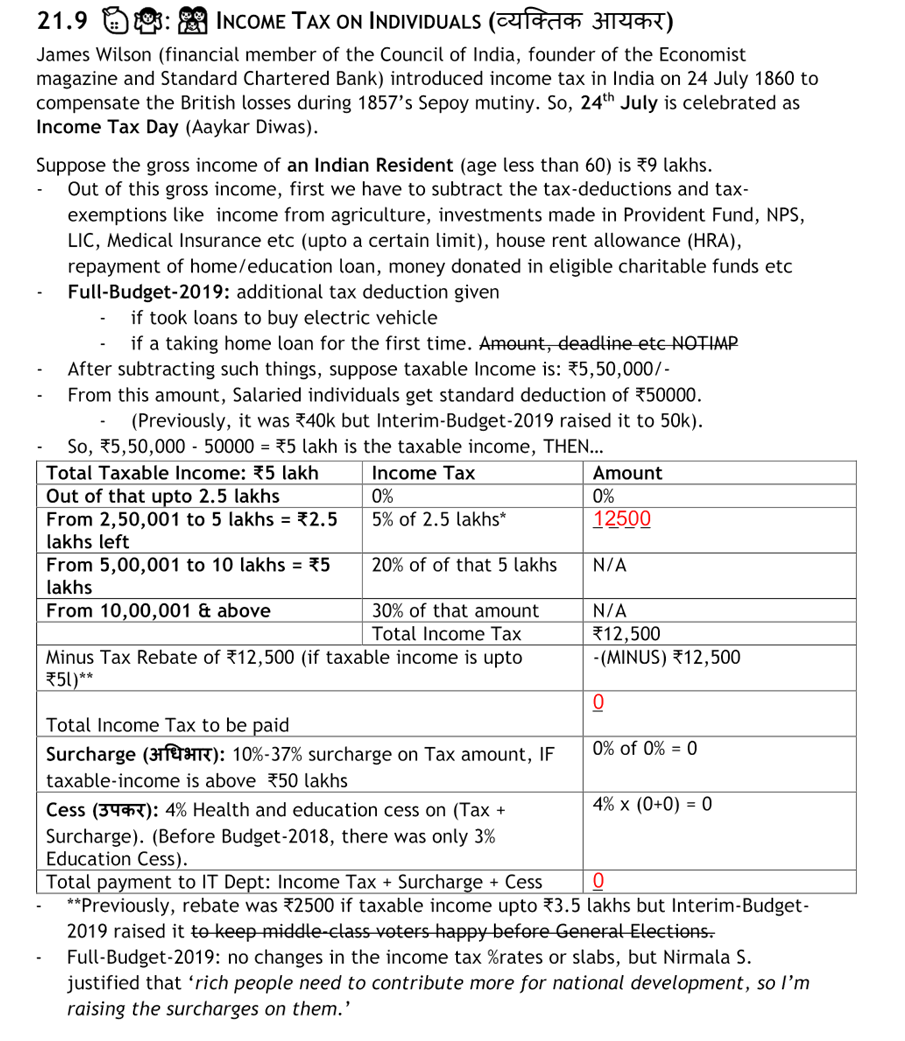

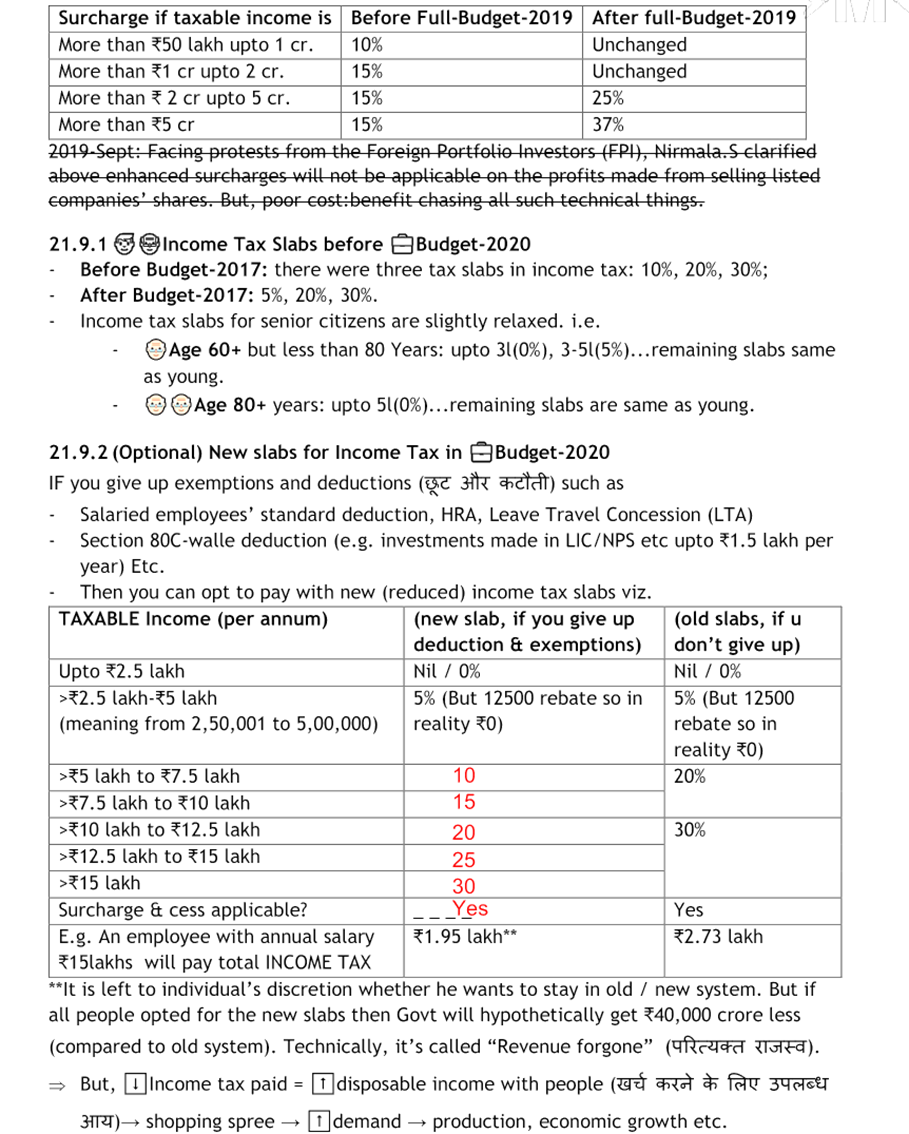

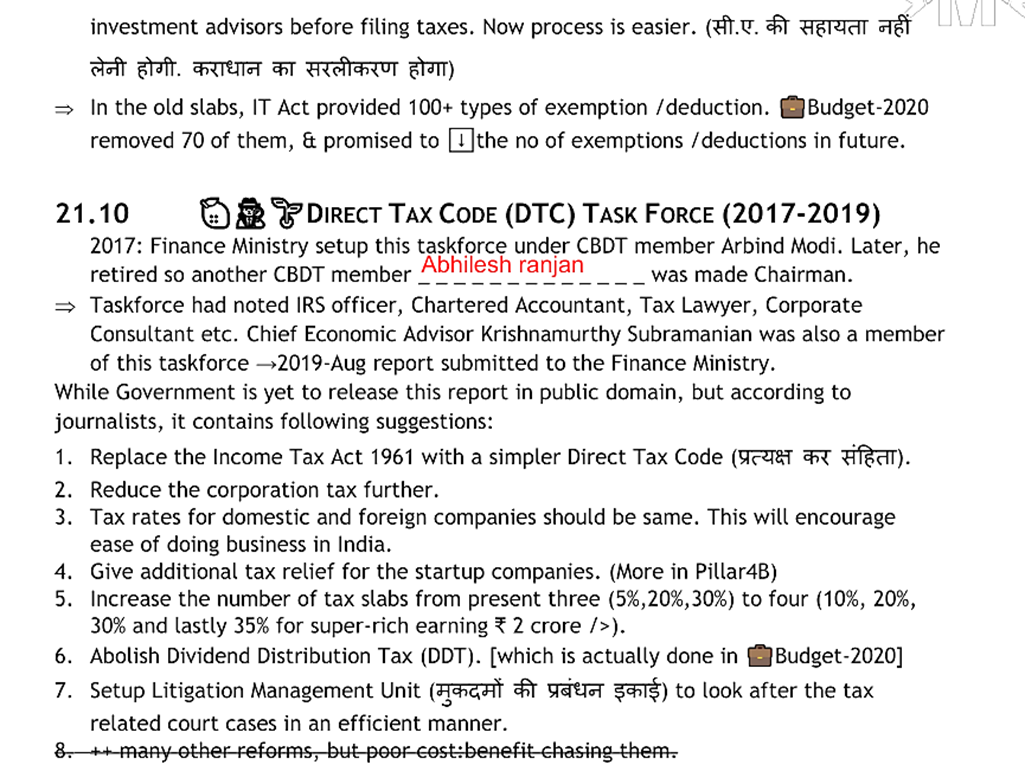

A Finance Bill is a Money Bill because it contains inter-alia taxation proposals and matters connected therewith or incidental thereto. The Rajya Sabha cannot pass or reject it. But it can amend it.

TAX

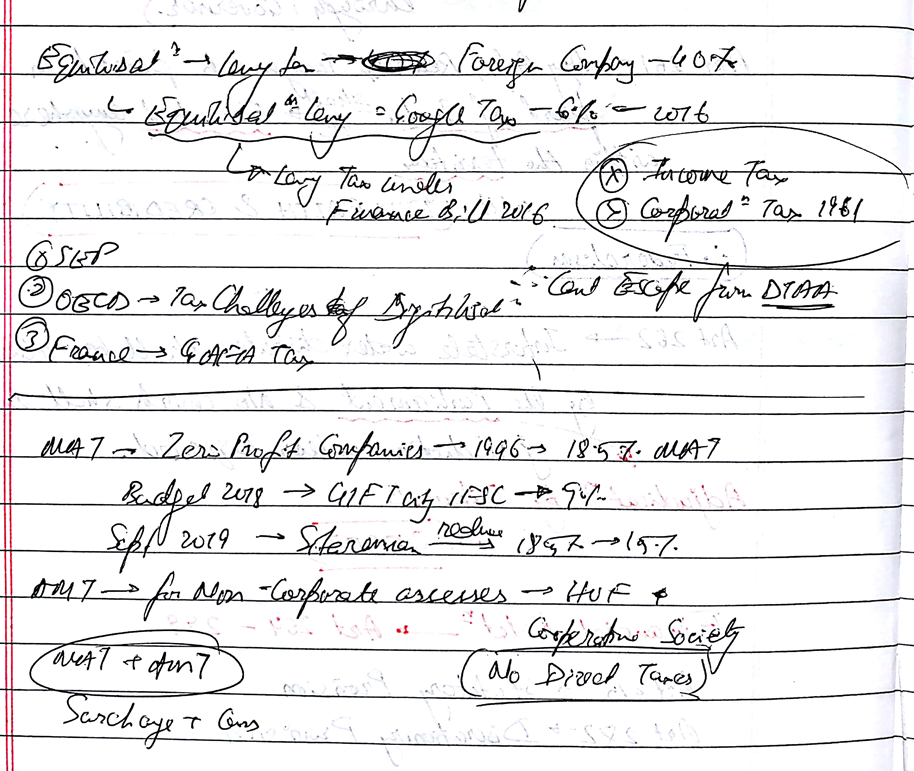

Equalisation Levy is a direct tax, which is withheld at the time of payment by the service recipient. The two conditions to be met to be liable to equalisation levy:

- The payment should be made to a non-resident service provider;

- The annual payment made to one service provider exceeds Rs. 1,00,000 in one financial year.

Equilisation Levy Tax– Some Digital platforms/ adsense companies have their server in a country with low tax. They might earn money from Indian users.. but dont have to pay taxes in India. In 2016 India became the 1st country to levy a tax of 6% on the lines of BEPS.

BEPS

Base erosion and profit shifting (BEPS) refers to tax avoidance strategies that exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax locations.

2020–> Indian Budget–> Equilisation tax –> besides online Ad services, it levied on e-commerce operators crossing the prescribed threshold, for supplies to Indian residents, persons using an Indian IP.

Why pursue this?- The equalisation levy was conceptualised as an interim measure to collect revenues and drive global negotiations. It was always acknowledged as an unsustainable levy complicating the taxation framework. Policymakers initially viewed this complication as a fair trade-off for short-term revenue gains.

Problem–

- Double Taxation

- Questioned constitutional validity and compliance with international obligations.

- 2020 amendment led the levy to wide and vague complicacy.

- amendments were never a part of the government’s Budget presentation and were introduced without consultation impacted investor sentiments

Budget 2021–> increasing the scope —

- they ‘clarified’ that ‘e-commerce supply or services’ include a plethora of online activities.

- ‘Online sale of goods and provision of services’ that qualify an organisation as an e-commerce operator was proposed to include the following activities undertaken online — acceptance of offer for sale, placing of purchase order, acceptance of purchase order, payment of consideration and supply of goods or provision of services, partly or wholly.

- ‘consideration received from e-commerce supply or services’, now also included consideration for sale of goods and services irrespective of whether the e-commerce operator owns the goods, or provides the services.

negatives–

- It also complicates the regime by on one hand exponentially widening the tax base, and on the other allowing exclusions. This amendment also does not address the apprehensions caused by the changes first proposed through the Finance Bill. This includes the coverage of e-commerce operators that only make offline businesses accessible digitally, and those that do not charge commission.

- Frowning Foreign Investors–> Finance Act, 2021 introduces all amendments to the scheme as ‘clarifications’ applicable since April 2020, which could be in violation of the Constitution. Foreign investors typically frown at such amendments.

- additional compliance burden increases platforms’ costs, which are eventually recovered from customers.

FinMin–> Dept of Revenue–> CBIC–> unveiled a Secure QR coded Shipping Bill that would be electronically sent to exporters.

fulfilling its commitment to a Faceless, Paperless, and Contactless Customs under the umbrella of its “Turant Customs” programme.

- Green Customs

- improving India’s ranking in the World Bank’s “Trading Across Borders” parameter of its Ease of Doing Business (EoDB) index.

- Would be implemented in phases across the entire country by 1st January 2021.

CBIC–> launched Information Technology (IT) initiatives – ICEDASH and ATITHI.

CBIC–> 1% Cash Payment norms is applicable to all the 45,000 taxpayers. This is being introduced to curb tax evasion by fake invoicing. The CBIC has so far booked 12,000 cases of Input Tax Credit fraud

- mandatory for businesses with monthly turn over of over Rs 50 lakhs.

- restricts the use of Input Tax Credit (ITC) to discharge GST liability.

- These norms are not applicable to taxpayers where the registered person has received a refund amount more than Rs 1 lakh or if the partner has paid more than Rs 1 lakh as income tax.

- The 1% cash payment norms have been included in Rule 86B of the GST

According to CBIC, out of the total GST taxpayer base of 1.2 crores, only 4 lakh taxpayers have monthly supply value greater than Rs 50 lakhs. Of these 4 lakhs, only 1.5 lakh taxpayers pay less than 1% of their GST liability in cash. When the new rule is applied, the 1% tax payment in cash will apply only to 40,000 to 45,000 tax payers. This will be 0.37% of the total tax payers of 1.2 crores.

CBIC–> Amendment–> Customs (Import of Goods at Concessional Rate of Duty) Rules, IGCR 2017 to boost trade facilitation

procedures and manner in which an importer can avail the benefit of a concessional Customs duty on import of goods required for domestic production of goods or providing services.

- imported goods have been permitted to be sent out for job work. Importers can now get the final goods manufactured entirely on job work basis.

- help MSME sectors

- allow those who import capital goods at a Concessional Customs duty to clear/re-sell them in the domestic market on payment of duty and interest, at a depreciated value.

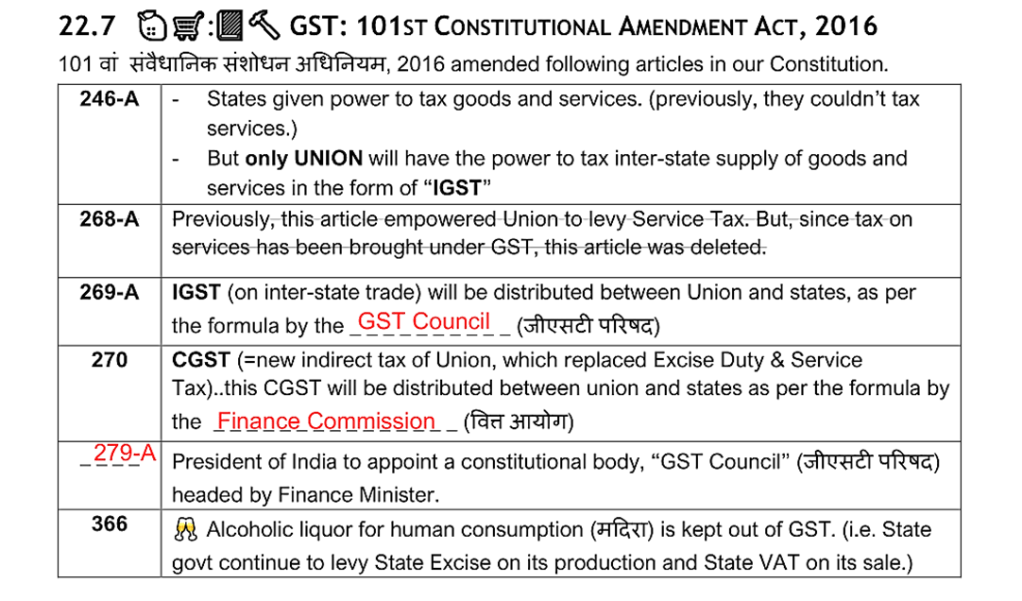

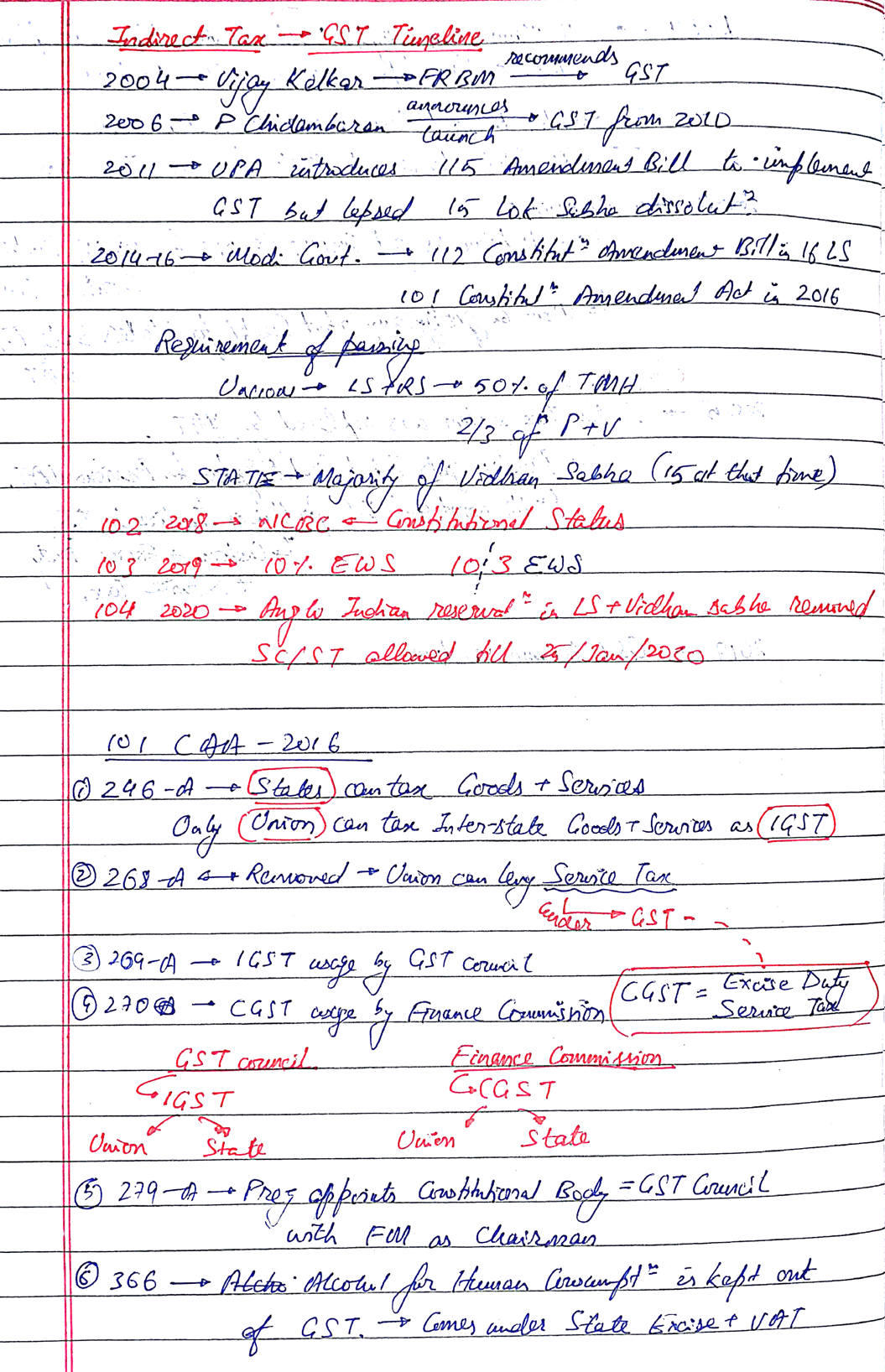

GST

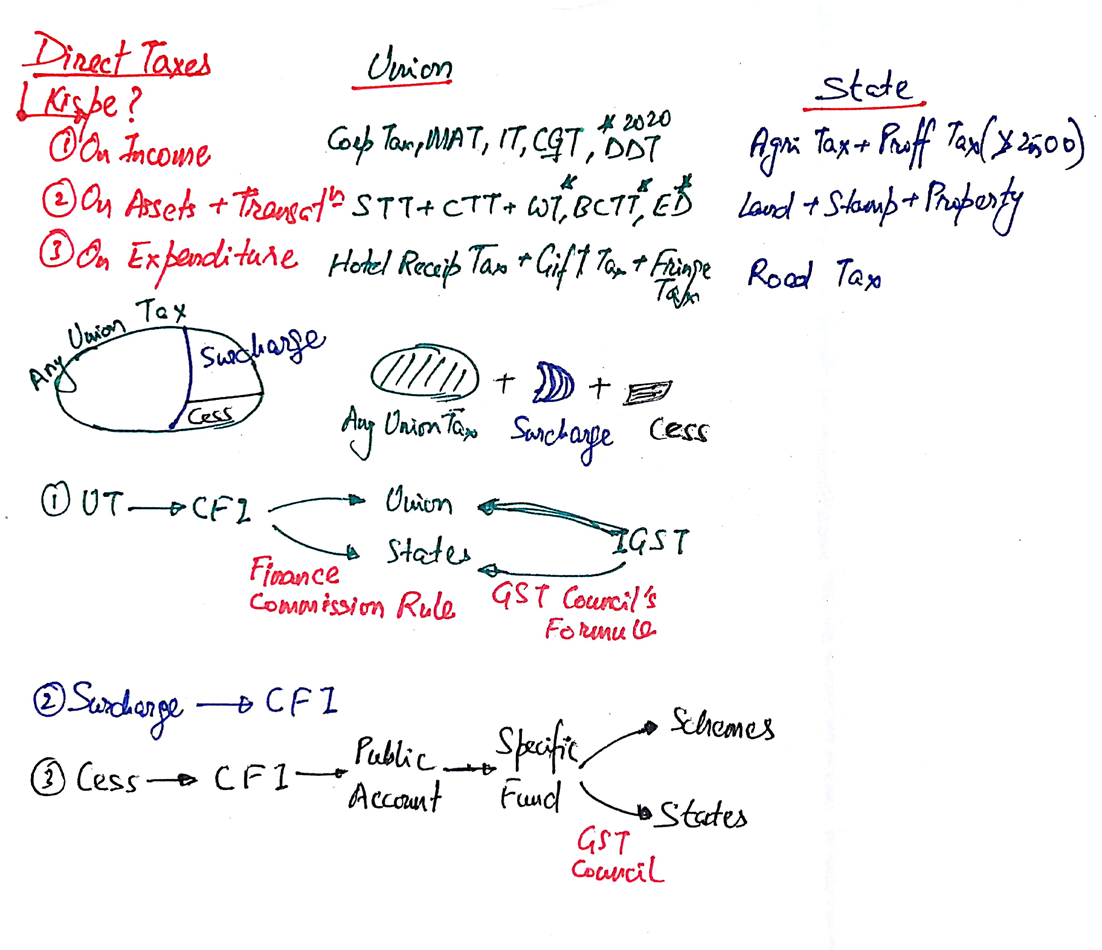

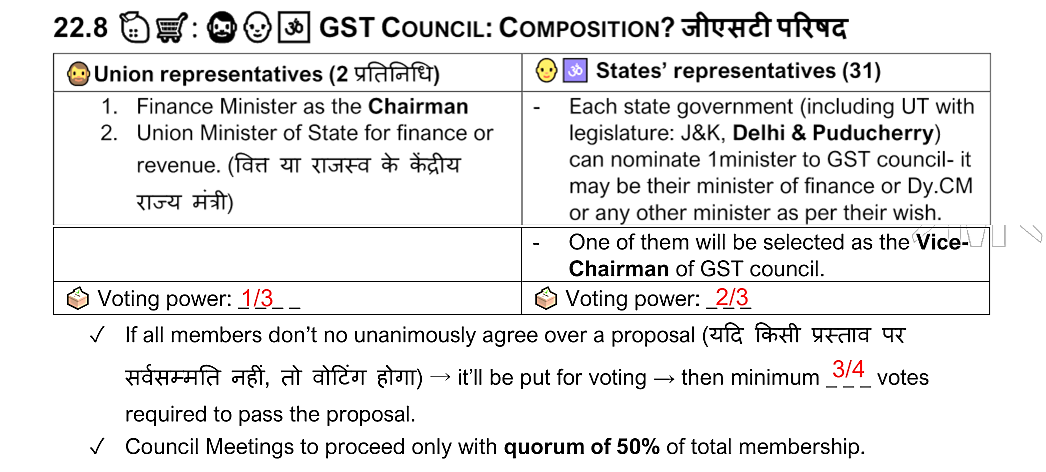

Art 280– Prez appoints Finance Commission (Quasi-Judicial body) headed by FM.

GST Council– 33 members–> 2 from union + 31 from States +UT

- Finance Minister as the Chairman

- Union Minister of State for finance or

revenue

Voting power: 1/3

31– Each state government (including UT with

legislature: J&K, Delhi & Puducherry)

can nominate 1 minister to GST council- it

may be their Minister of Finance or Dy.CM

or any other minister

Voting power: 2/3

GST Council: Functions?

- List the indirect taxes to be subsumed by GST regime.

- Decide the date from which Crude oil, Petrol, Diesel, Aviation Turbine Fuel and Natural Gas will be put under GST regime.

- Decide Standard rates for GST

- Decide Special rates for GST–> during natural disaster / calamity if required. E.g. 2019- Jan– allowed Kerala to levy a 1% calamity cess on intra- state trade for next 2 years, for the rehabilitation of 2018’s flood-victims.

- Integrated GST (IGST) system during interstate commerce

- GST registration of businessmen. If Bizman has turnover >40lakhs, he must register @GSTN online portal, he must collect GST from consumers and deposit it there.

- Protecting the interests of the special category states i.e. 8 NE states and Himalayan states (Himachal + Uttarakhand.

- Compensation to the states for their revenue loss in switching from VAT to GST regime via CESS mech.

- Dispute settlement between Union vs state(s), state(s) vs state(s)

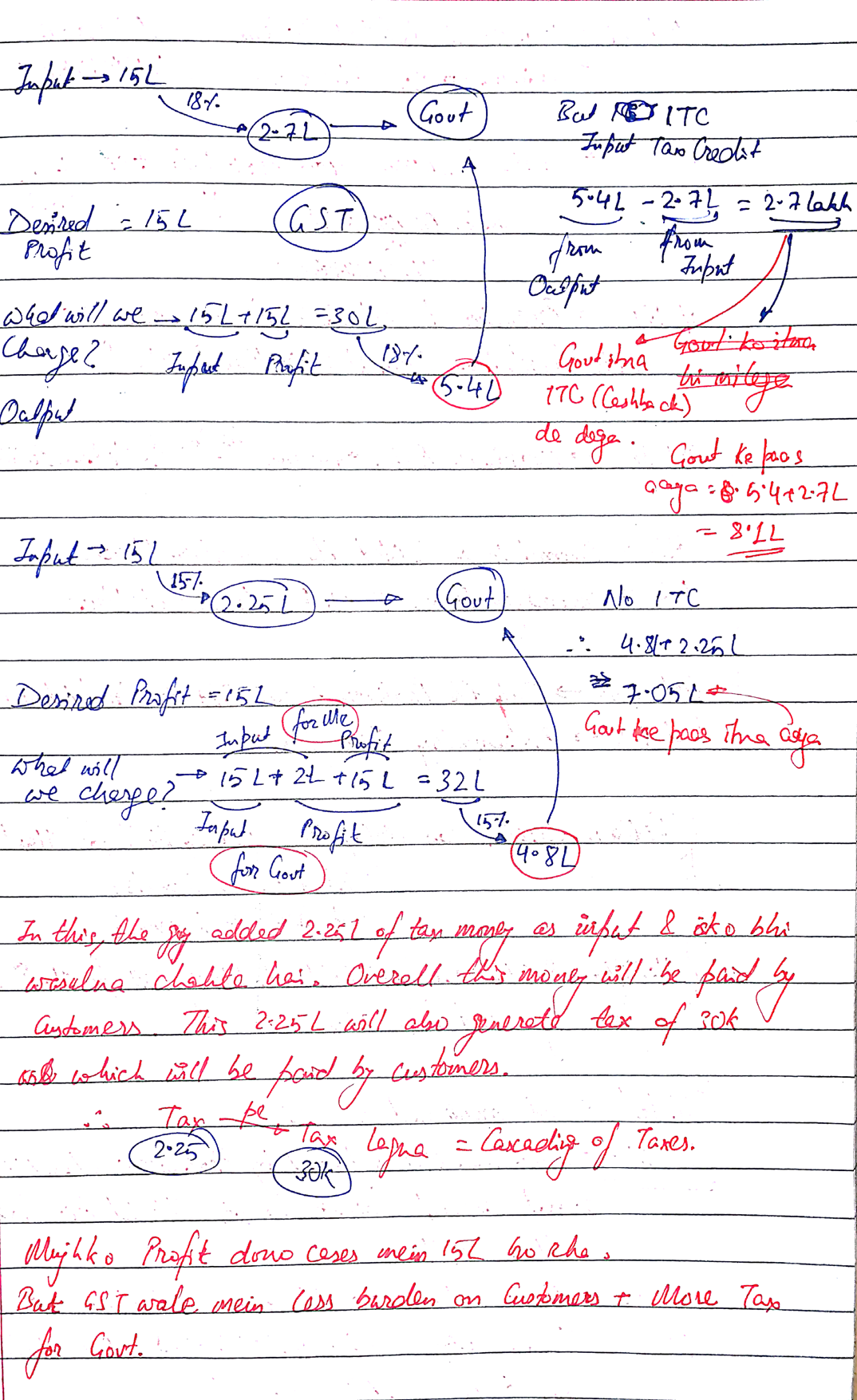

GST INPUT TAX CREDIT = ITC

GST is a ‘destination based’ indirect tax on consumption of goods & services

Intra-state supply–

Union levies→CGST

Inter-state supply–

Union levies→IGST

Cross-utilization of ITC :

- IGST credit can be used for payment of all GST taxes.

- CGST credit can be used only for paying CGST or IGST.

- SGST credit can be used only for paying SGST or IGST.

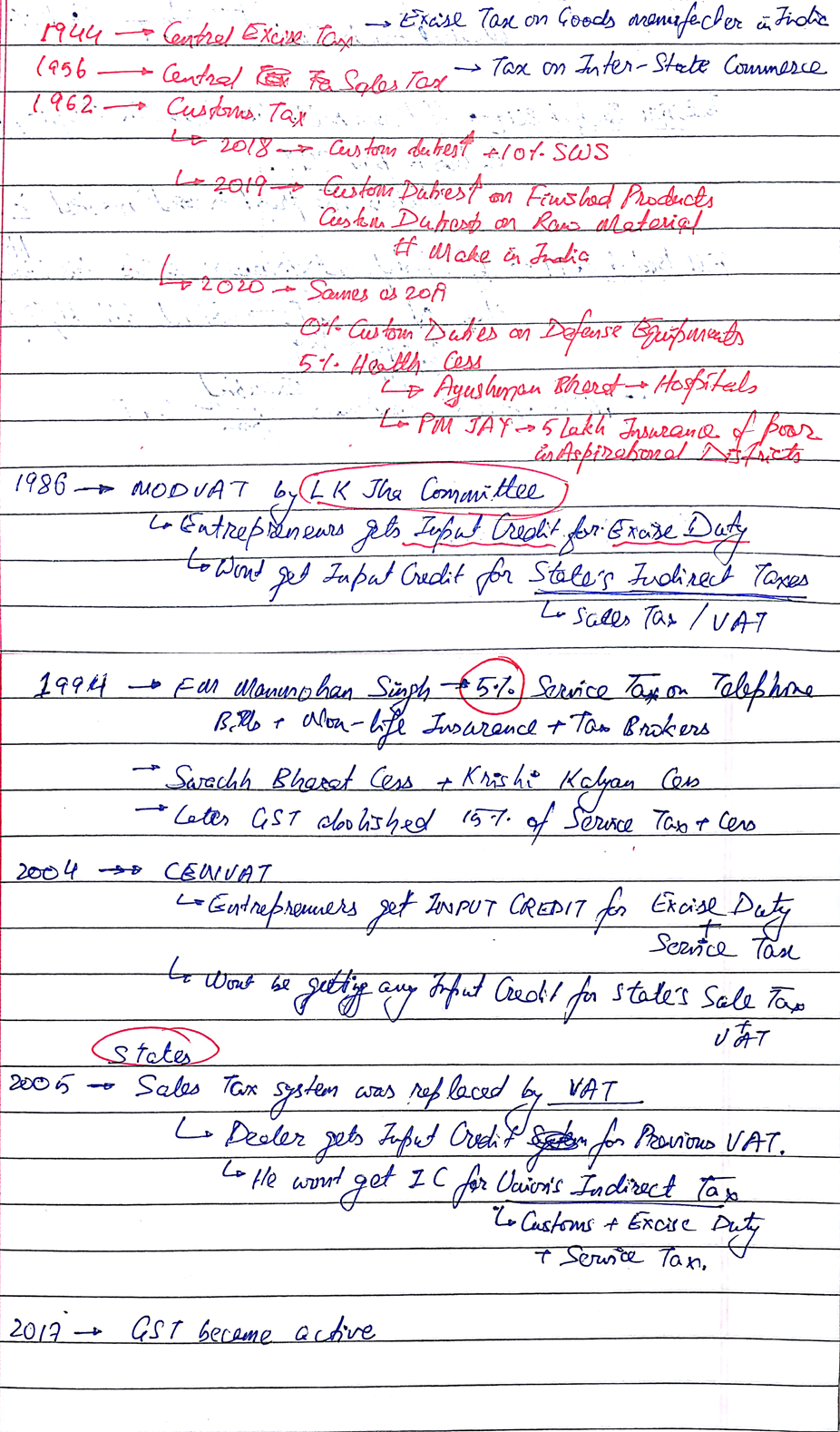

CENTRE’S INDIRECT TAXES SUBSUMED IN CGST

| For import-export: Basic Customs Duty, cess / Surcharge on it. | Custom Duty is separet from GST regime–> Customs duty + IGST Earlier— Customs Duty + Edu Cess 2018–Customs Duty + 10% SWS=Social Welfare Surcharge 2020— 5% heath cess on inpoterd medical device |

| Imports–> SAD + CVD | ABOLISHED |

| CST= Central Sales Tax | CST replaced by IGST= CGST + SGST |

| Services–> Service Tax+ KKS (Krishi Kalyan Cess) +SBC (Swatchh bharat Cess) | Completely replaced by CGST. |

| Manufacturing/ production of goods: Excise duty and various Cess / surcharges on it | Replaced by CGST (except 5 hydrocarbon fuels: petrol, diesel etc Manufacturing medicinal & toiletry preparations containing alcohol (e.g. Cough syrups, deodorants and perfumes) also replaced by CGST. Alcoholic Liquor for human consumption- falls in States’ purview so Union Excise / CGST not applicable on it. |

| Excise duty on Tobacco products | replaced with 14% CGST. Union also levies + GST Compensation Cess + NCCD (National Calamity Contingency Duty) National NCCD money–> Public Account–> Disaster Response Fund @ under Disaster Management Act, 2005. |

| Excise duty on production/refining of Crude oil, Petrol (Motor Spirit), Diesel, Aviation Turbine Fuel and natural gas | Once GST council decides the date they’ll be brought under GST-regime. currently–refineries / oil-drilling companies have to pay excise duty+cess/surcharges to Union for production / manufacturing of these items. (and petrol pump owner, etc will have to pay VAT to states on their sale. Presently, Petrol & Diesel are also subjected to Union’s Road and Infrastructure Cess–> Public Account–> Central Road & Infrastructure Fund @ under Central Road Fund Act 2000 |

Ministry of Finance recently announced that the businesses with annual turn over of more than Rs 5 crores will have to furnish six-digit HSN code on their tax invoices. The businesses with an annual turn over of less than five crores of rupees have to furnish four-digit HSN code.

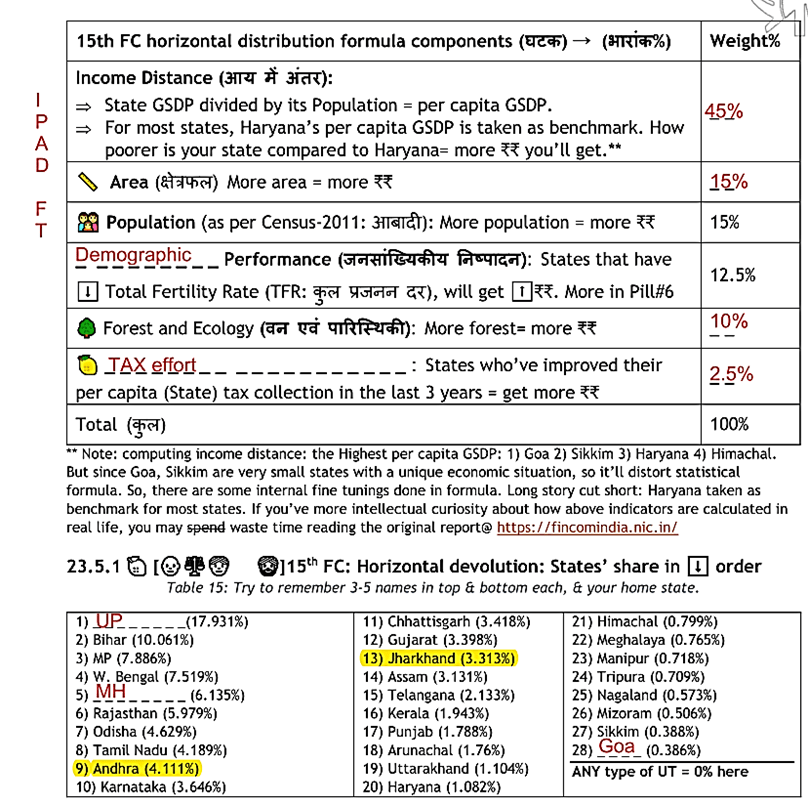

23.3.5 ✍🏻15th FC TOR: Conclusion (तनष्कषच)

✓ Economic Survey 2016-17 had observed ‘aid-curse’ in context of Redistributive Resource transfer (RRT) i.e. over the years, Special Category States received large amount of funds via Planning Commission and Finance Commissions yet couldn’t perform well in poverty removal or economic growth due to lack of accountability and poor governance.

✓ The 15th FC TOR aims to link the fund transfers with performance and accountability parameters. While states are apprehensive, but such measures are the bitter pills that we’ll have to swallow eventually to ⬆ India’s human dev. & economic growth.

Until 10th Finance Commission, the FC –> revenue sharing formula between the Union Government and Union Territories.

➢ But this practice stopped since 11th finance commission i.e. Finance ministry itself decides how much revenue will be shared with Union Territories based on its own discretion. Finance Commission no longer prescribed formula in this regard. But,

➢ 31st October 2019: The state of Jammu Kashmir was officially split into the union territories of Jammu Kashmir and union territory of Ladakh.

➢ Jammu and Kashmir Reorganization Act, 2019 mandates that:

o Whatever amount the former state of J&K was supposed to receive between 31/10/2019 to 31/3/2020 (as per 14th FC formula) …It will be distributed between these two new union territories on the basis of population ratio and other parameters.

o President of India shall require 15th FC to make award for UT of J&K. However, looking the 15th FC report, no separate share is given in verticle / horizontal tax devolutions. Simply 1% extra kept with Union to look after J&K & Ladakh.

23.6 🧔 → 💸🤲🏼 (👨🦲👳🏻♀ ) GRANTS FROM UNION TO STATES (संघ से राज्यों को अनुदान)

Apart from the tax devolution, FC would also suggest Union to give grant to the states

(grant= NOT loan, so need not return with interest).

14th FC suggested following types of grants→

- For All States: Grants for Panchayati Raj Institutions (PRI) and Urban Local Bodies

(ULB). These grants will be subdivided into two parts: basic grant and (10-20%)

performance based grants. - For All States: Disaster Management Grants.

- For 11 (कां गाल) States: Post-Devolution Revenue Deficit Grants (अंतरण-पश्च रािथि घाटा अनुदान) for ~11 States.

15th FC suggested following types of grants (in ⬇decreasing order, 2020-21)→

1) Local Bodies Grants (थथानीय ननकाय अनुदान, 90k cr)

2) Post-Devolution Revenue Deficit Grants (74kcr)

3) Disaster Management Grants (आपदा प्रबंधन अनुदान: 41kcr)

4) Sector Specific Grants: Nutrition (क्षेत्र-विलशष्ट अनुदान, ~7700cr)

5) Special Grants: (विशेष अनुदान , ~6700kcr)

6) Performance-based incentives (ननष्पादन-आधाररत प्रोत्साहन)